The 2026–27 Federal Budget has delivered some of the most significant proposed tax reforms Australia has seen in decades.

While some measures had been widely discussed in recent years, others came as a surprise — particularly the proposed changes to discretionary trusts.

Importantly, many of these measures are still proposals only.

The draft legislation, technical detail and interaction with existing tax law are still evolving, meaning there are areas where uncertainty remains.

As with all major tax reform, the final legislation may differ from the original announcements.

What is already clear, however, is that these proposed reforms could have a significant impact on:

For many Australians, the key issue will not simply be the changes themselves, but understanding:

The good news is that many of the proposed measures have long lead times and transitional periods, meaning there is still time for careful review and strategic planning.

Below is an overview of the major announcements and what they may mean for business owners, investors and families.

The 2026–27 Federal Budget contains a wide range of tax and business measures, however several reforms stand out as particularly significant.

From 1 July2027, proposed changes would limit negative gearing for residential investment properties to new builds only.

Existing residential properties held prior to 7:30pm on 12 May 2026 are proposed to be grandfathered, meaning they can continue under the current rules.

Under the new system, losses from affected residential rental properties would no longer be offset against wages or business income. Instead, those losses could only be offset against:

The Budget also proposes major reforms to capital gains tax from 1 July 2027.

The current 50% CGT discount for assets held longer than 12 months would be replaced with:

Importantly, these proposed changes apply broadly across assets — including shares, investments and property — and even extend to certain pre-CGT assets.

From1 July 2028, discretionary trusts may become subject to a minimum tax rate of 30%.

This could significantly affect traditional trust distribution strategies and the use of corporate beneficiaries (“bucket companies”).

The Government has also announced transitional restructuring relief for affected businesses and family groups.

The Budget also included several measures aimed at small businesses, including:

Additional measures for individuals include:

Negative gearing occurs when the income received from an investment property is less than the expenses relating to that property, resulting in a loss.

Under the current rules, the resulting tax loss can generally be offset against other income such as wages or business income. These rules have largely existed int heir current form since 1987.

Under the proposed changes from 1 July 2027, negative gearing for residential property investments will be limited to new residential builds only.

Importantly:

This means properties where contracts were entered into before the announcement time still qualify for grandfathering even if settlement occurs later.

The proposed transitional rules are particularly important.

Under the proposed system, losses from residential rental properties will no longer be offset against other income (such as wages or business income).

Instead, those losses could only be used against:

Where losses cannot be fully used in the current year, they would be carried forward and offset against future residential property income or gains.

For many investors, the proposed changes may significantly alter the long-term attractiveness of established residential investment property.

Potential implications may include:

Importantly, these changes do not commence until 1 July 2027, meaning investors still have time to review existing arrangements and long-term strategies.

At this stage, the legislation has not yet been finalised, so further detail and clarification is still expected.

Below are two examples of the current situation, compared to the proposed measure.

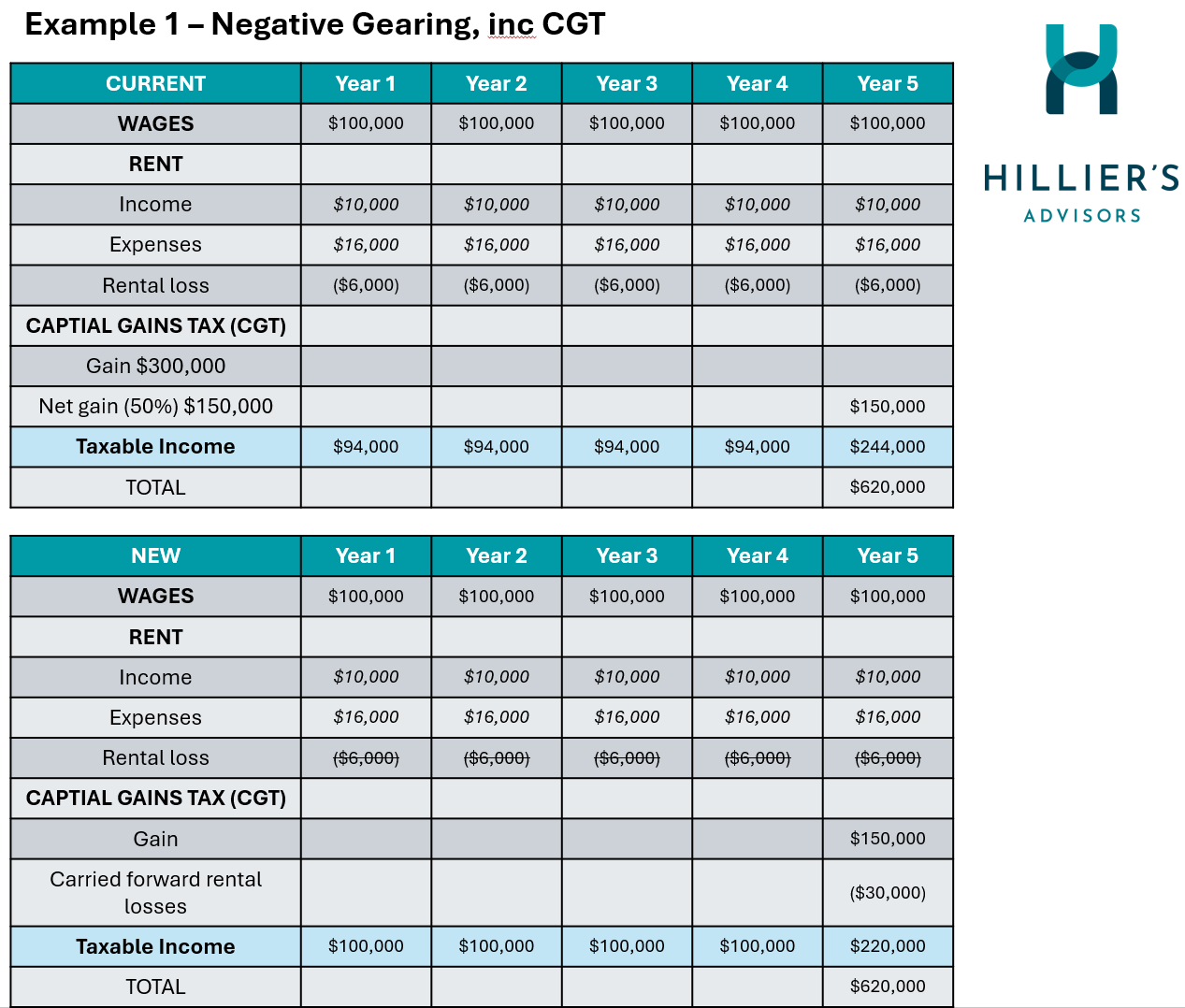

Firstly, an individual receives wages of $100,000 per annum, and a rental property loss of $6,000 per annum. In the 5th year, the property is sold for a gain of $300,000,

Under the current rules, the loss is deducted from the taxpayers salary each year. With the gain taxable in the 5th year.

In the second table, under the new rules tax is paid on the full $100,000 salary each year with the rental loss carried forward until it can be offset against the gain on the sale of the property.

You will note that over the 5 years, the taxpayer is taxed on the same total income however the timing differs. The end result may benefit some and disadvantage others, but the biggest challenge is the timing of the benefit of the negative gearing as many investors rely on their annual tax refund in order to service their investment loan and expenses.

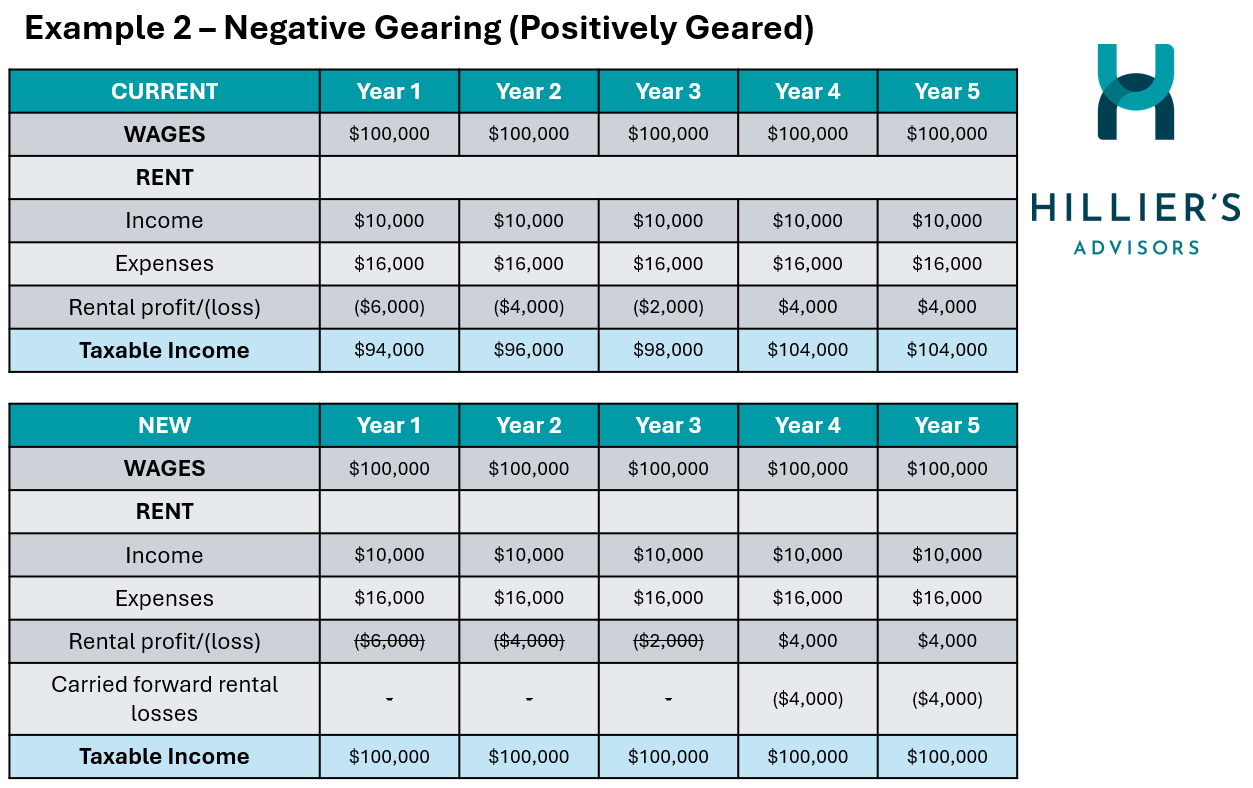

Our next example looks at where a property is initially negatively geared, but overtime as loan balances reduce and depreciation claims are utilized the property becomes positively geared. Similar to the first example, under the current rules each year the profit or loss from the rental is added to the other income received and taxed at their marginal rate.

Under the new rules, the losses incurred in the first few years are carried forward and then offset against the positive gains when they commence in year 4. Again, the overall income taxed over time will be the same, but the timing of the tax is different.

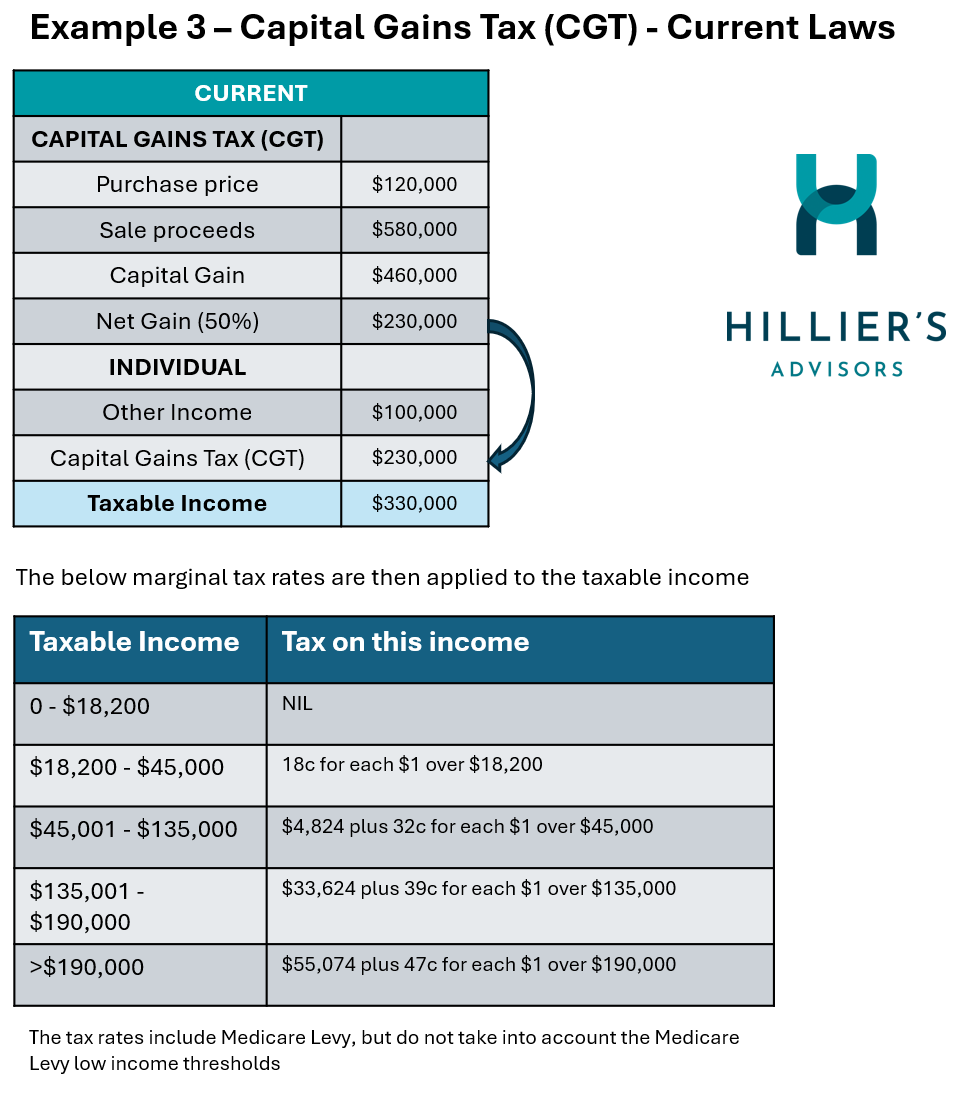

Capital Gains Tax applies when an asset is sold, examples of capital assets include shares, properties, businesses and various other investments. Capital Gains Tax was introduced in1985, prior to this date capital profits were not taxed. To this day, assets purchased prior to the commencement date (19 September 1985) remain tax free.

Since 1999, CGT has operated under the current rules where the gain is calculated by subtracting any purchase or sale costs from the sale proceeds. Where the asset has been held for greater than 12 months, a 50% discount is applied to the gain. The net gain is then included in the taxpayers taxable income and individual marginal tax rates are applied.

The below example demonstrates the laws as they stand currently:

Under the proposed changes from 1 July 2027, capital gains will no longer be eligible for the 50% CGT discount.

Importantly:

The proposed transitional rules are particularly important.

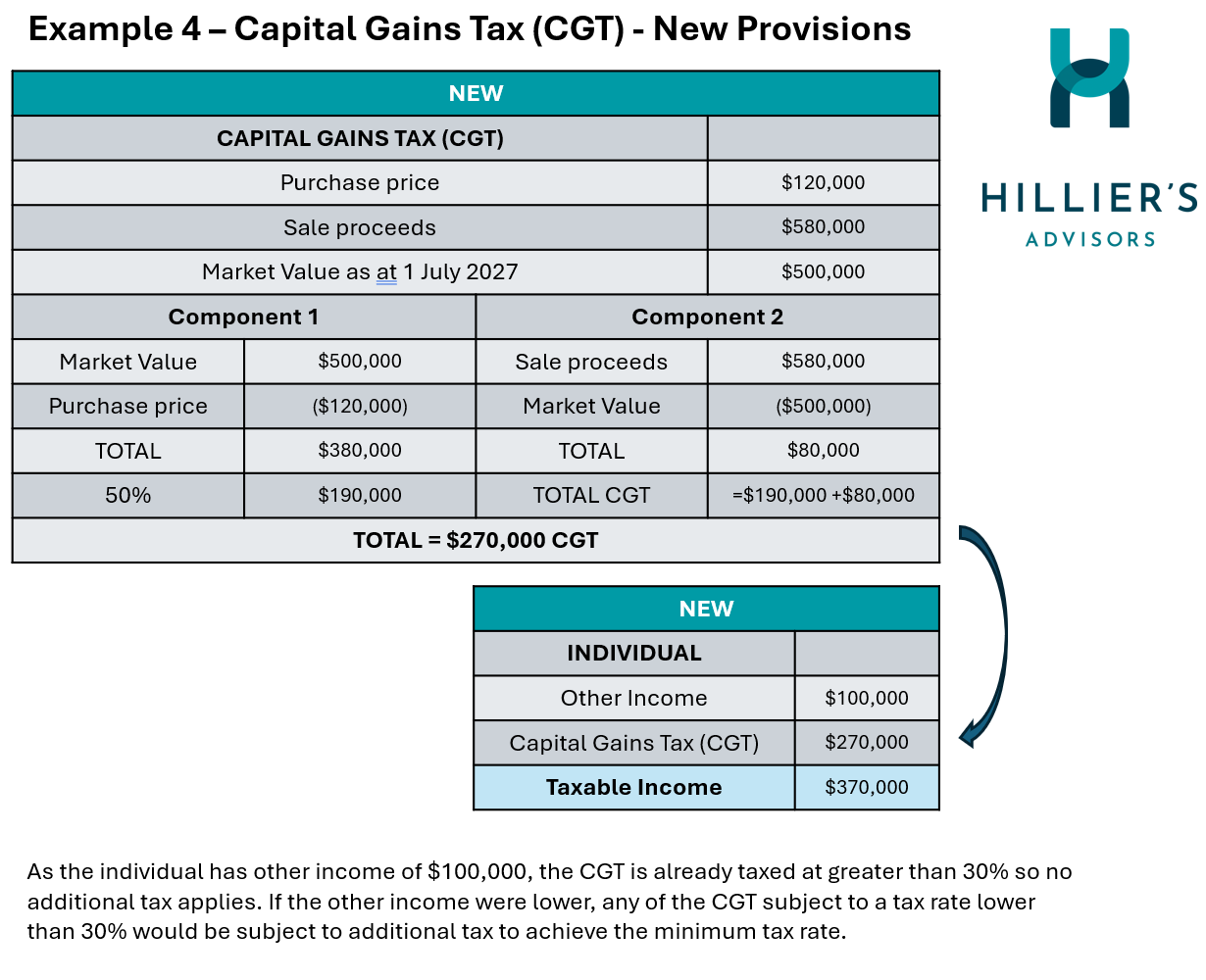

For assets owned prior to 1 July 2027 and sold after this date, the gain may effectively be split into two components.

The current CGT discount rules would generally continue applying to gains accrued before 1 July 2027.

Any growth occurring after 1 July 2027 may instead be subject to:

This means the market value of assets at 1 July 2027 may become extremely important for future tax calculations.

The example below shows the calculation of gains under these transitional measures.

Because future gains depend on the asset’s market value at 1 July 2027, obtaining reliable evidence of market value could become increasingly important.

The ATO will be providing guidelines of methods available for valuing assets for this purpose, so a paid valuation report will not necessarily be required. However, some substantiation of the market value relied upon will be essential.

Depending on the asset type and circumstances, taxpayers may wish to consider:

The calculation of capital gains is unchanged, but instead of applying the 50% CGT discount to the gross gain, indexation will be applied to the gain instead.

Indexation is designed to remove the effect of inflation from the gain, so that tax is only payable on the ‘real’ gain achieved. While the details are yet to be released, it is usually calculated by reference to the CPI figures relevant to the time of the sale compared to the time of the purchase. Indexation will only be applicable where the asset has been held for greater than 12 months.

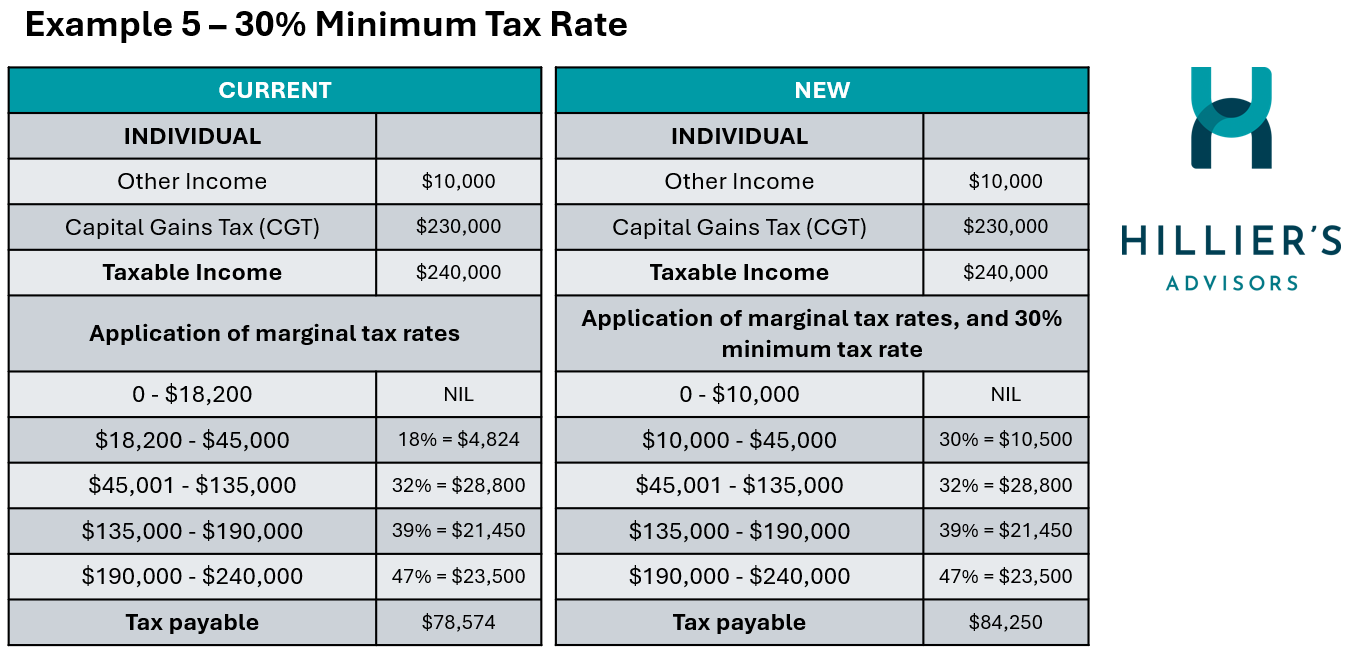

In addition, a new 30% minimum tax rate’ will apply.

In addition to indexation, introducing a 30% minimum tax rate on capital gains is proposed.

This is particularly significant for taxpayers who would otherwise have benefited from lower marginal tax rates.

While many technical details remain unclear at this stage, in effect, the minimum tax may reduce the advantages of:

Individuals receiving means-tested support payments, such as the Age Pension or JobSeeker, will be exempt from the minimum tax.

The below example shows how the marginal tax rates are applied to a capital gain currently, compared to applying the 30% minimum tax rate.

Under the new provisions, as the taxpayer only has other income of $10,000 the minimum 30% tax rate must apply to the full capital gain. Even though they have not fully utilized their tax free threshold or the lower tax bracket of 18%, the income is taxed at 30% until the marginal rates exceed this level.

Historically companies have been an unpopular choice for holding capital assets, due to a company’s ineligibility for the 50% discount. However with the removal of the discount, and with the 30% minimum tax rate not applying to companies, we may see the use of companies for holding capital assets increase. A company can apply a tax rate of 25% if it is classified as a Base Rate Entity (BRE), this definition requires less than 80% of the company’s income to be passive income(i.e. investment income as opposed to business income).

Importantly, these changes are not proposed to commence until 1 July 2027.

That means there is still time for investors and business owners to:

However, given the scale of the proposed reforms, early strategic planning may become increasingly valuable.

One of the most significant announcements in the 2026–27 Federal Budget was the proposed introduction of a minimum tax rate for discretionary trusts.

From 1 July 2028, the Government proposes that discretionary trusts will be subject to a minimum tax rate of 30%.

For many business owners, investors and family groups, this may represent a substantial change to long-standing tax planning and income distribution strategies.

Under the current system, discretionary trusts distribute income to beneficiaries each financial year. That income is then taxed in the hands of the beneficiary at their applicable tax rate.

One of the historical advantages of discretionary trusts has been flexibility.

Trustees can often distribute income between family members and entities based on:

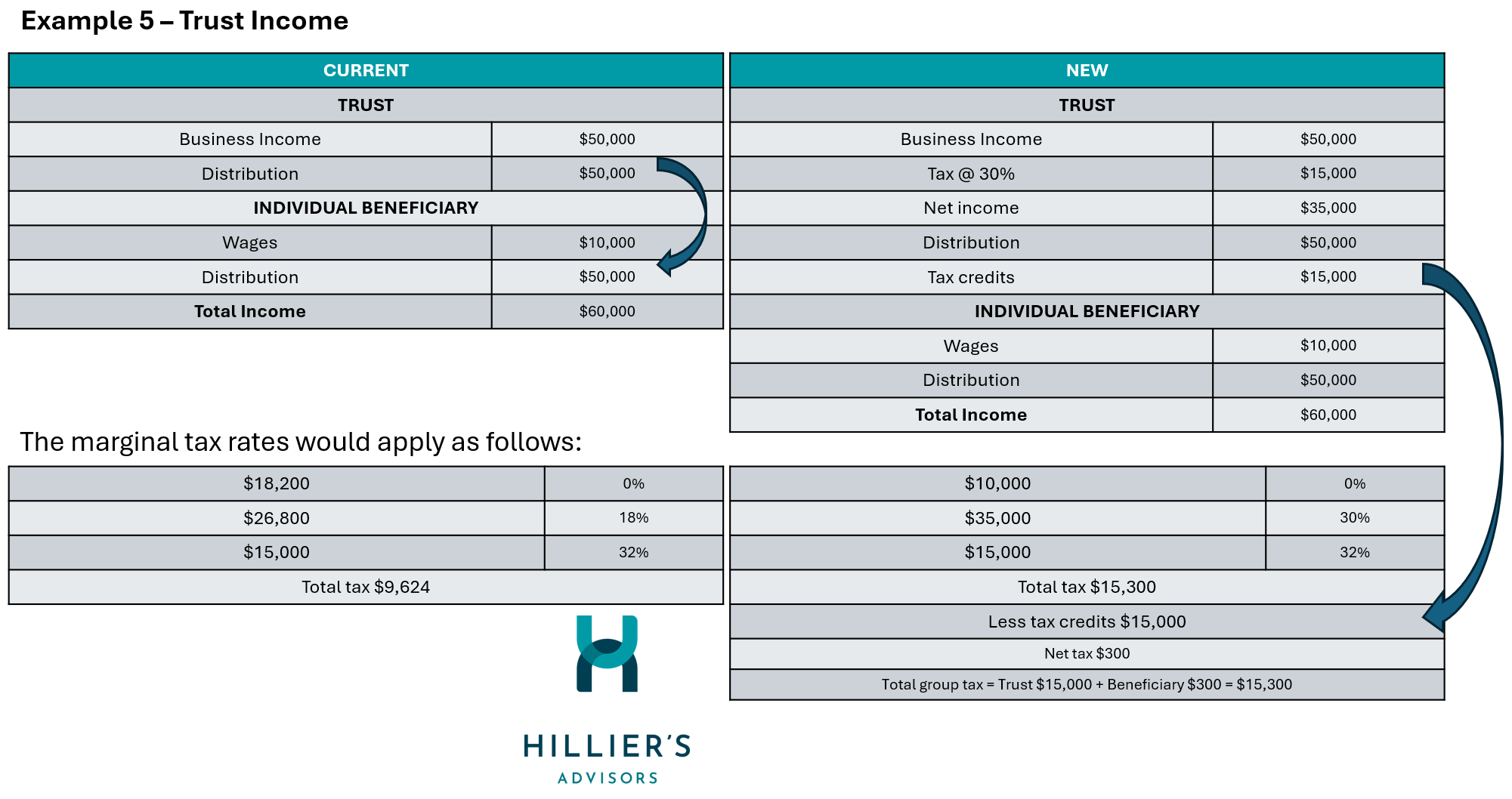

Under the proposed changes, discretionary trusts would become subject to a minimum 30% tax rate from 1 July 2028.

The trustee will pay the minimum tax, with beneficiaries receiving non-refundable tax credits for the tax already paid.

The is demonstrated in the example below, the current example showing the trust distribution of $50,000 including in the beneficiaries taxable income and taxed at their ordinary rates. Whilst under the new law the Trust pays 30% ($15,000) tax on it’s profit, before distributing the profit and credits to the beneficiary.

The proposed minimum tax is not intended to apply to all trusts. At this stage, exclusions are proposed for a number of types of trusts notably fixed trusts, superannuation funds and deceased estates. There are also proposed exclusions for certain types of income, including primary production income, and certain existing testamentary trust arrangements.

One area likely to become important is how the legislation ultimately defines:

These definitions do not always align neatly across different areas of tax law.

As a result, the final drafting and interpretation of the legislation may become critical in determining:

One notable aspect of the proposal is the impact on corporate beneficiaries, commonly referred to as “bucket companies.” As corporate beneficiaries will not be entitled to the credits for tax paid by the Trust, any distribution made to a company would be double-taxed.

Will this be goodbye to the well used tax minimization strategy of the ‘bucket company’?

Recognising the potential impact of the reforms, it has also been announced that expanded restructuring rollover relief will apply for year years commencing 1 July 2027.

Whilst there are minimal details at this stage, it suggests that relief will apply to eligible taxpayers restructuring from a discretionary trust to a fixed trust or a company.

This may provide important planning opportunities for affected business groups and family structures.

While the major structural reforms have attracted most of the attention, the Budget also included several measures aimed at individuals and workers.

From the 2027–28 financial year, the Government has proposed introducing a new $250 Working Australians Tax Offset.

The offset is intended to apply to individuals earning:

The Government has indicated the offset will apply automatically when tax returns are lodged.

Also proposed, is the introduction of a $1,000 instant tax deduction for work-related expenses from the 2026–27 income year.

Under the proposal eligible taxpayers will not need to itemise or substantiate deductions below $1,000,

However, taxpayers who incur more than $1,000 of deductible work-related expenses would still be able to claim their actual expenses under the existing substantiation rules.

This will replace existing simplified deduction thresholds, including the current $300 work-related expense threshold, and the $150 laundry expense threshold.

Certain deductions may still be claimable separately in addition to the instant deduction, including:

If the total claimable work related expenses exceed $1,000, the taxpayer can opt to use their actual, substantiated claim instead.

The Government has also announced proposed changes to the Private Health Insurance Rebate.

Currently, the rebate increases once taxpayers reach certain age thresholds. Under the proposed reforms, the age-based uplift would be removed from 1 April 2027.

This would effectively result in taxpayers receiving the same base rebate percentage regardless of age.

The Budget also included measures aimed at supporting businesses, improving cashflow and modernising aspects of tax administration.

The instant asset write-off threshold was previously due to reduce back to $1,000 after 30 June 2026.

However, the Government has now proposed making the $20,000 instant asset write-off permanent for eligible businesses with turnover below $10 million.

From 1 July 2027, businesses may be able to opt into monthly PAYG instalment reporting and payment arrangements.

The Government has also proposed allowing ATO-approved PAYG instalment calculations to integrate directly with accounting software (i.e. Xero, MYOB).

The intention is to better align PAYG instalments with real-time trading performance rather than relying on historical estimates.

The Government has also indicated businesses with a history of non-compliance may eventually be required to move to more frequent reporting.

From 1 July 2026, companies may be able to offset current-year losses against taxable profits from prior years and obtain refunds of tax previously paid.

From 1 July2028, eligible start-up companies may also gain access to refundable tax offsets linked to company losses. The proposal applies to the first two year’s of a company’s trading. However refunds are limited to the value of Fringe Benefits Tax plus Tax Withheld from wages.

The Budget also included changes to the Fringe Benefits Tax treatment of electric vehicles.

Under the current rules, eligible electric vehicles may qualify for full FBT exemption where:

Under the proposed changes:

Importantly, the treatment remains unchanged based on the purchase date of the vehicle.

Additionally, the discount is delivered by applying a 15% statutory fraction (instead of 20%), which is a method of calculating FBT based on the cost price of the vehicle. This means that where the vehicle has high business use, the log book method may give a more beneficial result.

With many of these reforms still in proposal stage, the most important step for many taxpayers right now is not rushing into major decisions.

Instead, the focus should be on:

As the proposed changes are confirmed and become law, it will be important to seek advice as to how your specific circumstances are affected.

The CGT changes in particular make access to the small business CGT concessions more valuable that ever. Anyone potentially eligible for these concessions should be reviewing their structures and planning ahead to ensure eligibility when the time comes. It is important that this is done ahead of time, as some tests require conditions to be met for as much as 7.5 – 15 years.

Anyone holding assets subject to capital gains tax, should consider how the asset will be valued at 30 June 2027 and ensure adequate substantiation of the valuation used is available.

One of the most important things to understand is that many of these reforms are still proposals only.

While the announcements are significant, the legislation is still evolving and many technical details remain unclear.

For most taxpayers, this is not a situation requiring rushed decisions — it is a time for informed planning.

Many of the proposed reforms do not commence until:

In addition, many measures still require:

That means there is still time for considered planning rather than reactive decision-making.

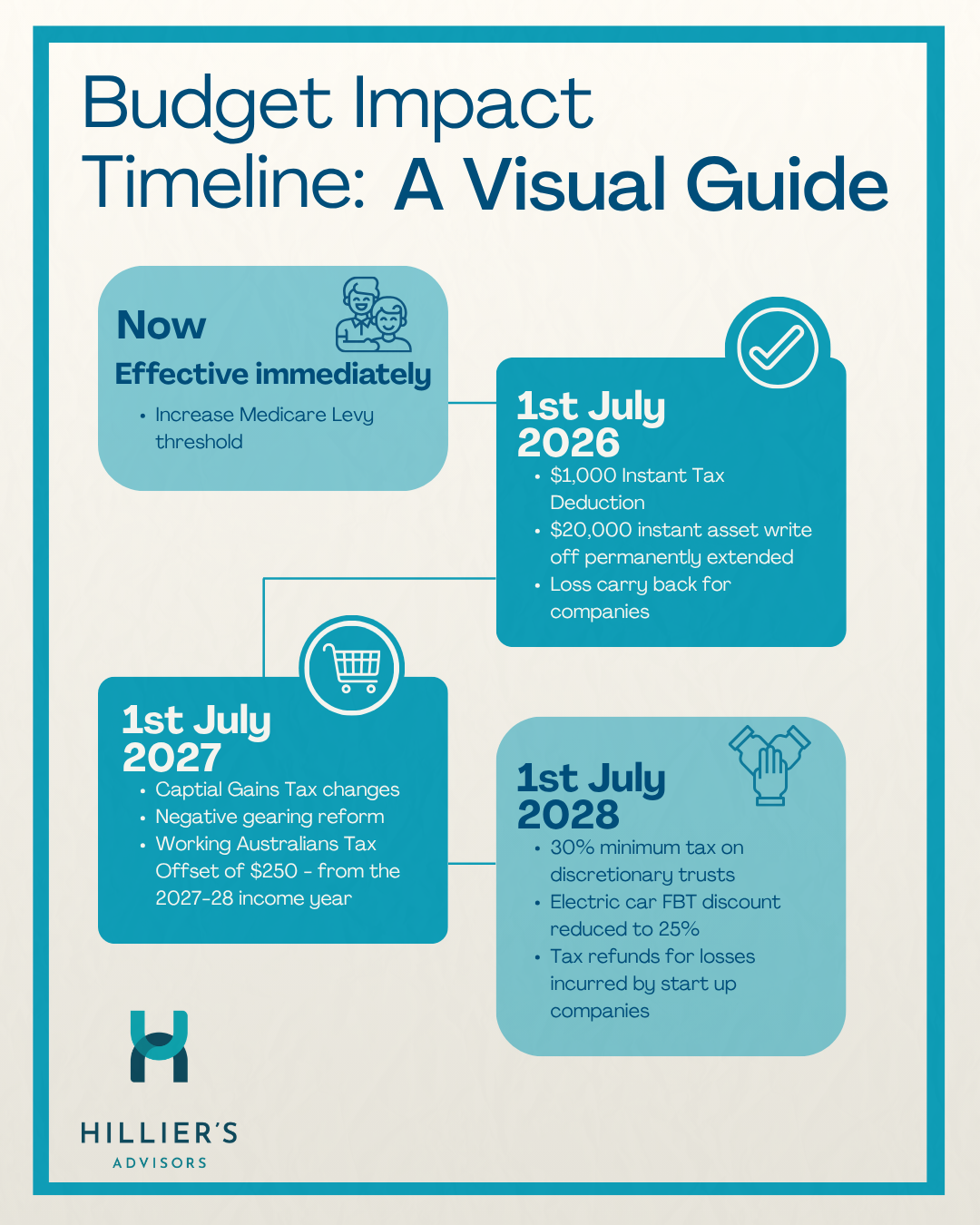

Our Budget Timeline below summarises the effective dates of the major announcements.

Since 1989 Hillier’s Advisors have been delivering financial services to individuals, businesses and business owners across Newcastle and the wider Hunter Region. A major focus for the Hillier’s Advisors team and the work we do is providing the right financial advice when our clients need it, not just when they ask for it.